Most merchants discover they’re on the MATCH list the hard way: a new processor approves them, then reverses days later with no clear reason. The account is gone before anyone explains why.

What MATCH actually is

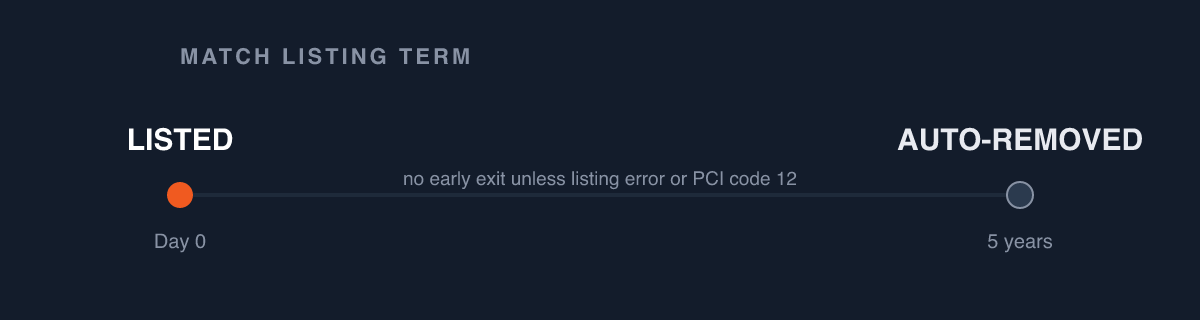

MATCH, Mastercard’s Member Alert to Control High-risk Merchants (the database once known as the Terminated Merchant File), is a shared blacklist acquirers check during underwriting. When an acquirer ends a merchant relationship for a serious reason, it’s required to add the business, tagged with a numbered reason code (excessive chargebacks, suspected fraud, PCI failure, and so on). A listing lasts five years, then drops off automatically.

Why you can’t remove yourself

Here’s the part that catches people out: you cannot petition Mastercard directly. Only the acquirer that placed you on MATCH can request removal.

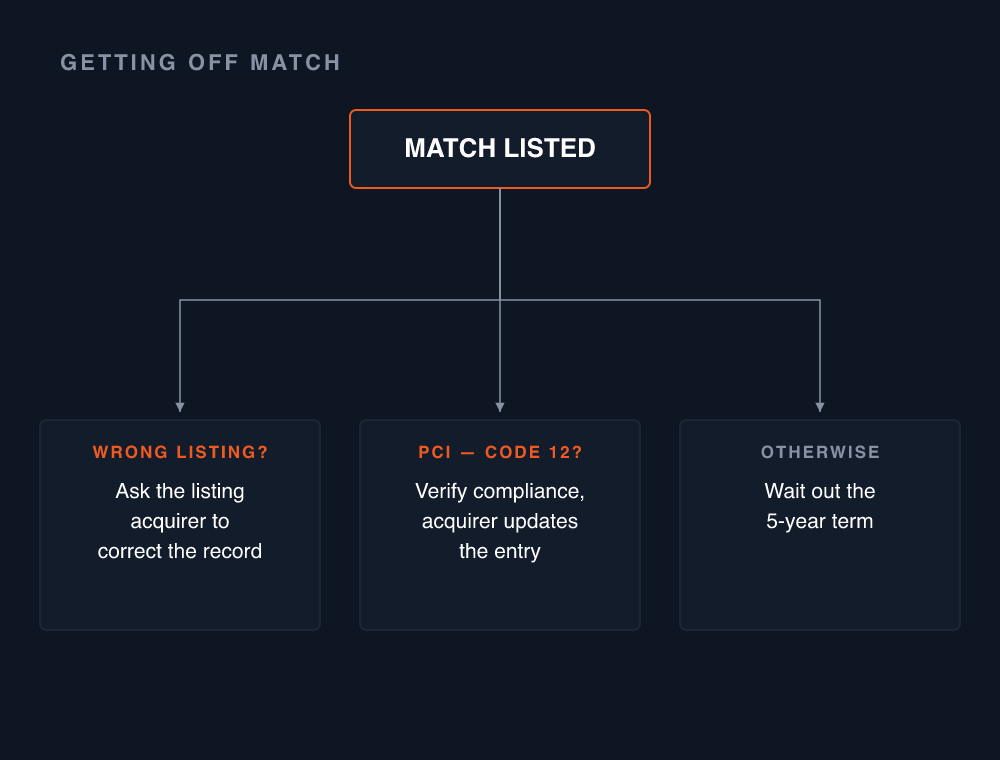

The paths that actually work

Early removal exists in narrow cases:

- Wrong listing. Misidentification, an incorrect reason code, or an administrative error: ask the listing acquirer to correct the record.

- PCI compliance (reason code 12). Once you demonstrate you’ve remediated and are compliant, the acquirer may update the entry.

Outside those, the five-year clock runs.

What to do now

Get your record and exact reason code from the acquirer that listed you. You can’t fix what you can’t see. If the listing is wrong, document everything and press that acquirer in writing. If it’s valid, fix the root cause (usually chargebacks or fraud controls) and, in the meantime, work with high-risk acquirers who knowingly underwrite MATCH-listed merchants.

MATCH isn’t a life sentence, but it’s rarely a quick one. The lever is the bank that listed you, not Mastercard.